How To Make A Simple Boat Budget and Save Money Faster

You’ll get where you’re going faster by doing your budgeting research

Saltwater Journal is reader supported.

When you buy through our links we may earn an affiliate commission (at no extra cost to you)

Budgeting isn’t a glamorous side of boat life. But it’s an important one — regardless of your income size. Because no matter how much money you have coming in, you need to know what your costs are and how much you’re spending. So you want to know how make a simple budget, and save up or pay off debt quicker right? I know what it’s like to just want to get out there on the water now. A well thought out budget is key to achieving your cruising goals. It doesn’t have to be fancy — you just have to know what costs to put in it, and how to stick to it.

Here I’ll share everything I’ve learned about making a simple boat budget in 5 easy steps and the best tips to save faster. I’ll also share my secret budgeting tool I’ve used since 2018. This is awesome for anyone who wants to keep track of their dollars easily in real time, without tricky spreadsheets. So if you’re a beginner budgeter, or saving to buy your first boat, or fund a live-aboard lifestyle read on!

We were broke students but we wanted to buy a boat

When I met my husband we were both full-time post-graduate students, my daughter was at primary school and we were renting our home. We had part-time jobs but money was super tight. We grew what we could in our backyard and were creative in living thrifty. It was scary knowing there were no back-up funds if something major happened, and stressful not feeling financially secure (what that looks like is different for everyone). For us, it means having a reliable income source and not stressing about money — having our bills covered, with savings for emergencies and a modest investment scheme for retirement.

Upon graduation, we started new jobs and began looking at ways we could create a lifestyle we love — we wanted to live on a boat and travel. But with no savings, we were starting from scratch. I knew we needed a plan. Aside from coming up with the initial funds to buy a boat, we needed to know whether we could afford to live onboard in a marina, while we paid back a boat loan, and covered boat maintenance and our usual living costs.

I started using the programme You Need a Budget to manage our money and it’s been a game changer. It’s helped us to:

Keep track of our incomings and outgoings without having multiple bank accounts to separate funds

Determine whether we could afford to buy a yacht and live onboard in a marina, while we worked nearby

Buy a yacht, live aboard and save for an extended cruising season

Make achievable plans that work for us as a couple for the next few years

Read on for the most important things I’ve learned about how to budget simply and successfully. And whether you’re working with a small or large income — the principles are the same.

This step by step guide will help you think through your expenses, costs of boat ownership, and visualise what your goals are – so you can plan your life adventures and make them happen.

1. Set a goal

The first thing to making a budget that’s going to work for you, is to set a goal. Everyone’s life and financial circumstances are different but we all need to decide: What’s my budget for? What do I want to achieve?

Maybe you’re just getting by each day/week/month and you want to feel less stressed by being able to plan ahead. A budget can help you prioritise your most important expenses and know how much to put aside for rent, food, electricity, childcare (the list goes on).

Perhaps there’s a big life event you want to save for — a wedding, a house deposit or a trip overseas, and at the moment your spending is all over the place. You know you could save much more than you are and you want more control over your money.

Maybe, you want to figure out a new budget so you can make a life change — like transitioning from land to buying a boat, and living aboard. With some real focus, you know you can make it happen sooner rather than later. But just how soon?

Being clear on your goals will frame your money decisions around short-term and long-term spending.

2. Know your boating intentions

It might sound basic but it’s important to know: What are your intentions with buying a boat?

People buy boats for all kinds of purposes:

day sailing

summer cruising

living aboard in a marina

cruising full-time in your own country

sailing around the world

You need to choose a boat that’s going to suit your sailing needs. This will determine the type of boat you buy and how much you need to spend. Everyone has their own expectations around what kind of lifestyle they want with their boat and being clear on this will help you and your partner or family decide how much you invest. Plus the costs that are involved with that — which will go into your budget.

It’s also important to consider that you may transition through several boats before really knowing what works for you, what you like (or don’t like) before finding your ultimate boat — especially those looking to cruise around the world. That’s why it’s a great idea to get as much sailing experience as you can, across a variety of boats if possible, before buying your own.

Once you know what you need the boat for, you can start putting a list together of requirements you want in your first boat. If you’re just starting that process — read Beginner’s Guide to Buying a Boat.

3. Know your costs for your lifestyle

To put an accurate budget together, you need to know in good detail what your lifestyle costs are before you buy the boat. Start by writing down everything you know that you have to spend money on during the year. This can be a daunting experience when you add up all the ‘actual’ costs you have. But it’s the only way to really assess how much you spend. And how much you can afford. In the You Need a Budget app, it helps you sort your expenses into groups. Every time you get paid, you allocate each dollar to a category in one of the groups such as:

Immediate obligations

For us, this covers things like berth rental, monthly bills like phone/internet, personal insurances and software subscriptions for design work.

True expenses

These are the less frequent but actual things you need to spend money on during the year such as vet bills, taxes, sailing subscriptions, the dentist etc. Allocating money regularly to these types of expenses in your budget means that you don’t need to stress when the time comes to pay these — because you’ve already planned for it and have the money ready.

Debt payments

Having the ability to live-aboard and travel without debt hanging over your head is one of the ultimate freedoms. Be honest about what debt you have (especially any credit cards). Add it into your budget, and no matter how small your payments — keep paying it and reducing it. We’ve been focussing on clearing our student loan debt. This will make it far easier for us to travel overseas for a longer period of time, without having extra interest payments added.

Lifestyle

Account for your true lifestyle in your budget. If you enjoy dining out and know full well you plan to take advantage of the odd resort while you’re cruising — add these expenses in. There’s no point in excluding your real lifestyle expenses in your budget — or it won’t be accurate and you’ll end up under-estimating your costs.

Just for fun

Budgeting isn’t supposed to make your life all serious with no play! You can create a category in your budget for something enjoyable — that’s up to you. And it’s easier to stick to your budget long-term if you’ve got a little play money that’s a guilt-free spend too.

Boat expenses

We have a section that covers regular yacht costs and we allocate money to these categories each time we’re paid.

Boat costs to consider

These are some of the common expenses to factor into your budget with boat ownership— especially if you’ll be spending time in a Marina berth:

Berth rental

Mooring fees

Live-aboard fee

Power and water charges

Fuel costs — Gas bottle refills and diesel

Boat Insurance

Annual haul-out costs

Regular Maintenance costs

Planned upgrades Eg more solar, new rigging

Cruising Budgets

We found that our budget while we were living and working on land to pay off our boat loan was quite different to when we were cruising around New Zealand. While our income was lower when we were cruising, our expenses were too. We’d sold our car (no petrol, car registration, car maintenance etc), we didn’t have live-aboard fees or power invoices etc.

I highly recommend Lin and Larry Pardey’s book Cost Conscious Cruiser: Champagne Cruising on a Beer Budget.

4. Calculate how much you can spend on buying a boat

The amount of money you have to spend on buying boat will become clearer as you define your expenses and your boat requirements. How much you spend on your boat will also depend on the condition of it when you buy it, and how many upgrades you need/want to make.

A general rule of thumb is to allow 10% of your boat’s value annually for regular maintenance but upgrades are extra to this. Early on when we bought our first boat, we did some interior upgrades on a cheap budget, and spent more money investing in safety gear such as new life-jackets, a Safety Grab bag and EPIRB. We also made the yacht more liveable year-round by purchasing clear sides that zipped to the bimini, so that the cockpit was nearly fully enclosed. These were items we thought about when weighing up the boat we wanted to buy, and how much we could offer.

My top tips for determining your boat budget are:

Decide what type of sailing you’ll be doing and what you need from a boat — Eg will you be coastal sailing with your family of four, in warm climates during the summer only, keeping the boat in a marina? Or living aboard on your own, on anchor, planning off-shore voyages?

Do your research – find out what other boats similar to one you’re looking for are selling for — (new and secondhand), in your own country and in others. The more you build up a selection of boats to cross-reference, the more confident you can feel in setting a realistic budget for that age and style of boat.

Research costs involved with maintaining vessels. The condition of a boat is not always determined by its age — it also comes down to the previous owners maintenance routine and how well they’ve cared for and looked after it with regular work. But there are certain things you would allow for in your budget when buying an older boat — such as eliminating safety risks. An example would be rewiring throughout the vessel or updating battery connections if they’re old and no longer compliant. Many marinas require your vessel to have a certificate of compliance to show the electrical work is safe to connect to shore power. Marine electrical work can be pricey, so adding this into your boat budget is smart.

Expect more parts to break onboard than anticipated, and marine items will cost more than you think. Give yourself leeway in your budget to cover the unexpected.

5. Plan for how you’ll finance the boat.

There’s different ways to pay for a boat and each will have a different impact on how you budget:

Pay cash up front

The preferable option is paying for the boat outright. Maybe you hand over fat stacks of cash or drop a chest of pirate gold at the seller's feet, but a bank transfer is usually standard. Either way, if your boat is debt free you won’t need to budget for loan repayments or be subject to additional loan and interest costs.

Finance through a bank or finance company

Specialised marine lenders, banks and finance companies will consider lending you money for a boat. They’ll take into account your credit rating, income and value of the boat when deciding if they’ll give you a loan, and for how much. We found that it was difficult to borrow a large amount as an unsecured loan — that is, we didn’t have property or any large assets we could use to secure it, in case we failed to make payments. We also did some quick sums on the interest rate and couldn’t justify paying so much extra in interest — at the time, we were looking at 14% per annum! That’s a lot of interest paid over our 2 year repayment period.

Finance through alternative arrangements

Sometimes it’s possible to create an alternative loan arrangement that works for your situation. We negotiated a private loan of $40k from my parents, with a slightly better interest rate than what they were getting from the bank. Fair to say this was a good deal for them, and us — as it made for more affordable repayments.

Knowing our budget in advance ensured we were confident we could commit to the loan and keep my parents happy! We paid our boat loan back over a two-year period — which was quite an effort given we were also covering boat expenses in the Marina. That’s why our budget had such an important role to play. We lived as frugally as while we were students over those two years — but it meant that it was only a two year loan, and not four years! This allowed us to move onto our next goal.

Side Q&A: Why did we stay in a Marina for that time? Logistically it was our only option, as there were no suitable anchorages or moorings nearby to where we were working. Living in a marina helped us get to know our local boating community and learn to sail. Although many cruisers steer clear of Marinas to keep costs down and spend the time sailing, you need to do what works for you and your situation at the time. Sometimes, that means staying in one spot for a while.

Tip for borrowing money privately:

If borrowing money from family, always have the loan terms in written agreement signed by both parties (we did this with an outline of the repayment plan — dates and amounts etc). That way the expectations are clear for all parties. It’s also smart to have a lawyer review the agreement in place.

Looking for extra ideas on how to make money or for jobs that work well remotely? Check out 85+ ways to make money while cruising.

6. How to save up faster

A moodboard is a fun way of keeping you motivated to stay on track and achieve your budgeting goals

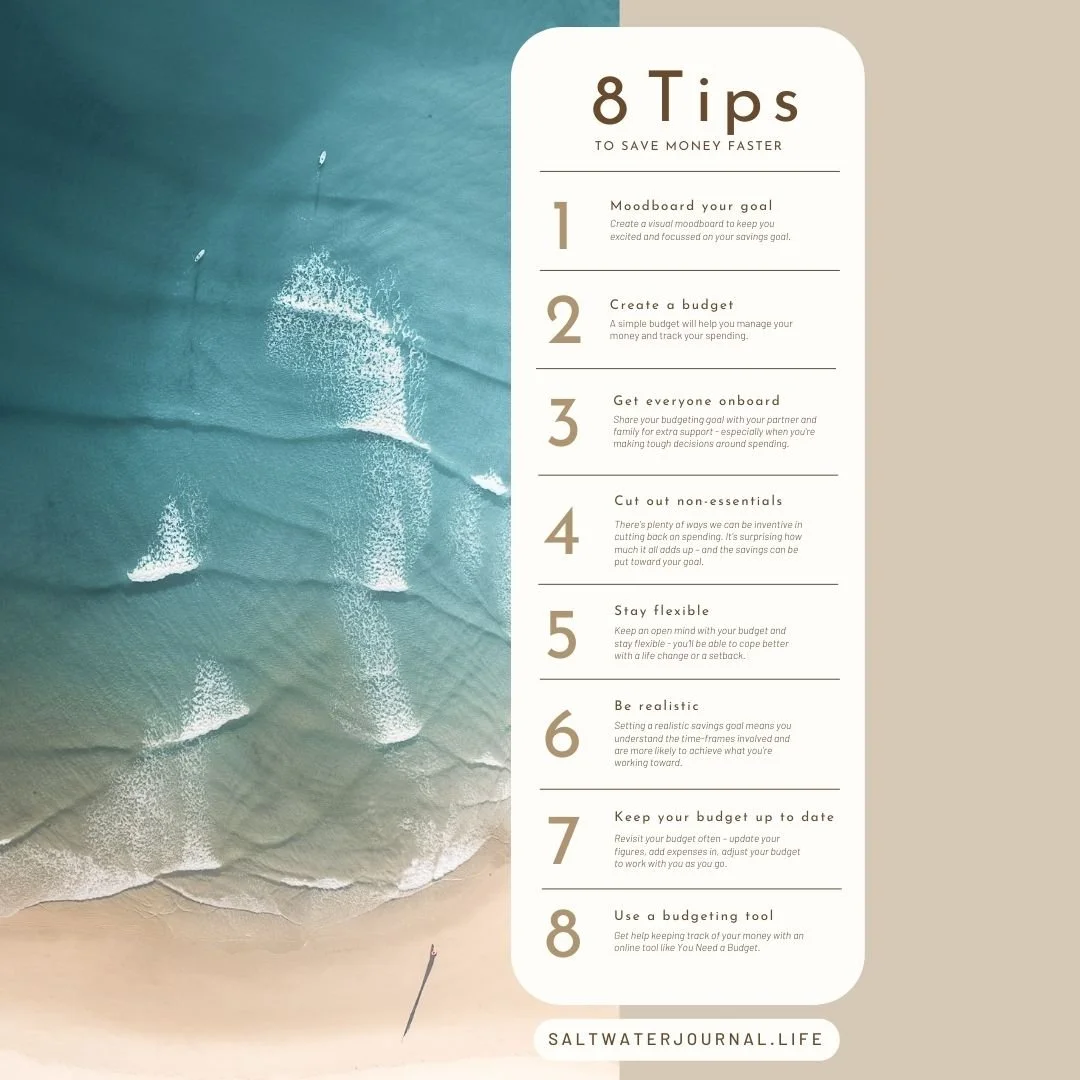

Create a moodboard for your goal

One of the keys to sticking with a budget is setting a goal for what you want to achieve. Maybe it's to buy a boat, or pay off a student loan, or clear a debt, or save for a year of cruising.

You’ll be more likely to make it happen if you know what you want and can focus on that. Because saving for something you really want can be hard and it takes determination. So a moodboard is a great way to keep yourself inspired! It can be digital or physical – Pinterest or Canva is a great way to collect visual ideas, or grab some magazines from a thrift shop and have fun snipping your way into a new life.

I created a moodboard with pictures of boats and sailing destinations that reminded me it was going to be worth it — especially when I had to make the choice between buying a bottle of red for $15 or saving that money. It all adds up! It’s also important to allow a small luxury every now and then (said bottle of cab sav) and that kept me going when it was tough. It’s amazing what you can achieve when you’re focussed on your goal.

Get everyone onboard

It’s much easier to change your life when your partner or family are in on the dream. The moodboard is awesome at communicating this! They’ll be more likely to lend support and understand why you’re saying no to a restaurant dinner out, or an event that’s outside your budget. You may discover some resistance from people in your circle who don’t understand why you’d want to make such changes or sacrifice ‘normal’ life for the sake of a new unknown adventure. But stick to what feels right — you know it’s worth a shot!

Cut out non-essential spending

Extra subscriptions, take-aways, cafe coffee, new clothes – there’s plenty of ways we can be inventive in cutting back on spending. It’s surprising how much it all adds up – and the savings can be put toward your cruising kitty.

Stay flexible

Life has a habit of throwing a spanner in the works just when you thought you had everything figured out! Health, family, relationships are all subject to change so if you keep an open mind with your budget and stay flexible you’ll be able to cope better with a change or a setback. Sometimes even better plans arise from a change in circumstances!

Be realistic

Setting a realistic goal means you understand the time-frames involved and are more likely to achieve what you’re working toward. If you’re like me, you want everything to happen now. You can just picture yourself sailing away and can’t wait for it to happen. Budgeting is a real test of patience and the rewards come over time (even if you’re saving as fast as possible). Perhaps you downscale some aspect of your boating dream, so that you can get out on the water sooner – gaining experience and giving it a go. See my book recommendation about that!

Keep your budget up to date

Revisit your budget regularly – update your figures, add expenses in, adjust your budget to work with you as you go. It’s a living thing and it doesn’t have to be complicated. But keeping it up to date will help you stay on track. And it’s much easier to reconcile where you’re at if you do it regularly. I find once a fortnight works well for checking in on ours.

Use a budgeting tool

Budgeting can be as simple or as detailed as you like. But if I’ve learned one thing over my years of saving — is that I need help keeping track of my money. It’s not because I’m irresponsible or spending out of control — it’s just that there’s a lot going on in life — and we all need the right tools to help us.

If you’re not into spreadsheets either, check out the programme You Need A Budget — it’s what I’ve used since 2018 and I swear by it.

It’s helped us keep track of all our incomings and outgoings,

taken the stress out of managing our budget

enabled me to see available funds we have to spend

given us detailed reports on how much we’re spending on the boat (and everything else)

allowed us to repay our boat loan quicker

given us back control of our money.

An example dashboard from You Need a Budget

I’ve used You Need a Budget since we were totally broke students and I still use it now that we’re working full-time and more financially comfortable. I don’t see us ever stopping — it keeps everything organised online without me having to keep it all in my head or on paper. It’s a subscription-based web app that can sync with your bank accounts (although since we’re with an Australian bank, I have to import my bank transactions but it’s easy to do).

Now we’ve paid off our boat, our goals are all about clearing our student loan debt and saving to prepare our yacht for offshore cruising.

Subscribe to You Need a Budget with my link and we’ll both get a month free - a win/win!

A personal note

There can be plenty of emotion and life stress tied up with managing money — whether it’s not having enough, trying to make more or planing how to use it — I understand that. It’s my hope that you’ll now have the motivation and tools needed to work on your own budget so that you can achieve your goals. Taking control of your financial situation does remove stress from daily life. Remember it doesn’t matter how big or small your budget is but the sooner you’ve got it underway the better you’ll feel!

Did you learn something about budgeting? Share it with someone else you think will find it helpful too…

Recommended

Discover the most extensive list of boat sale websites to help you in your search to buy a boat, and learn new places to look locally, nationally and world-wide.